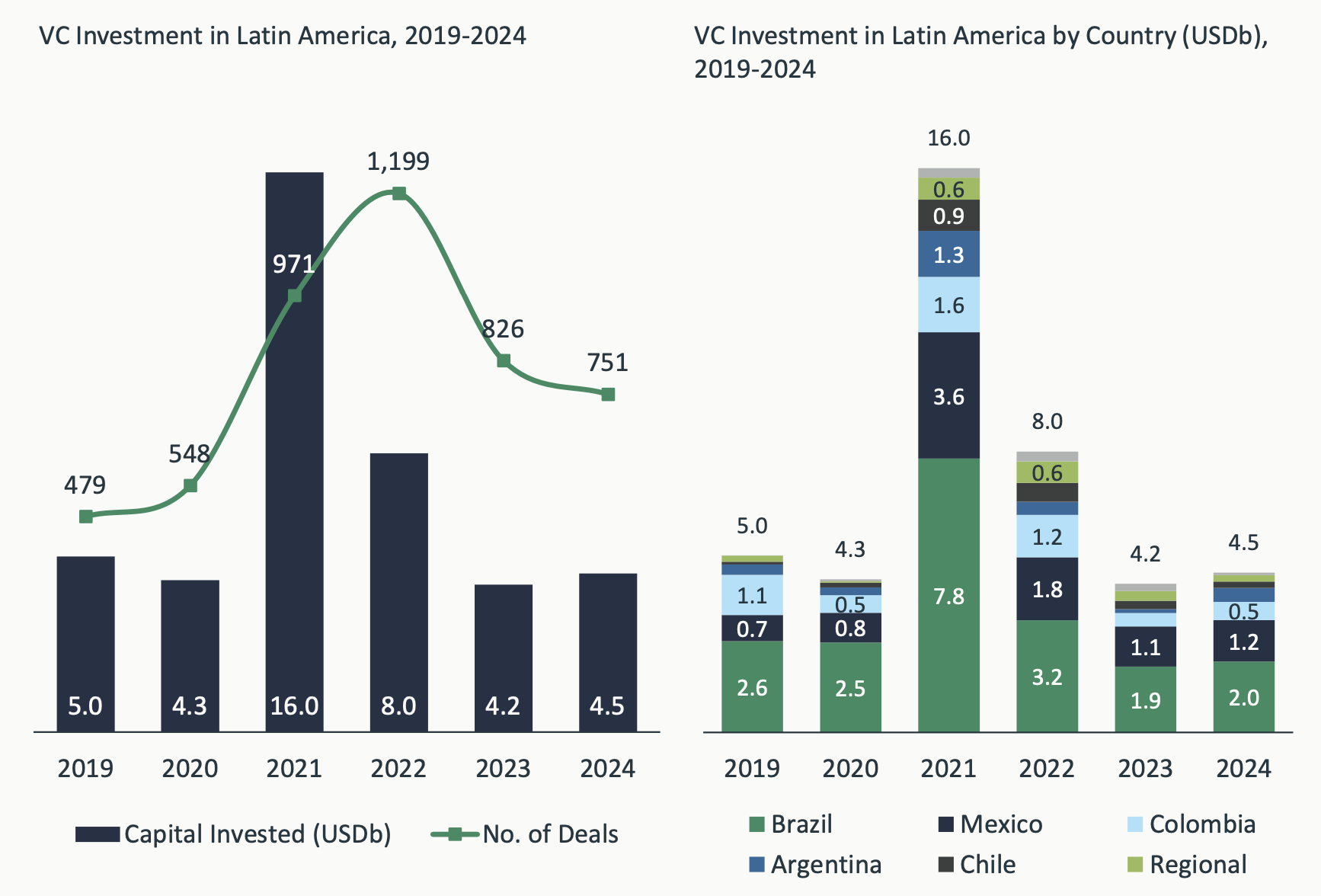

The Latin American venture capital market demonstrated resilience in 2024, stabilizing after the dramatic peak of 2021 and subsequent correction. According to LAVCA’s latest industry report, venture capital investment in the region reached $4.5 billion dollars across 751 deals, marking a moderate 8% year-over-year increase and signaling that the market adjustment phase may be behind us.

Investment Levels Holding Steady

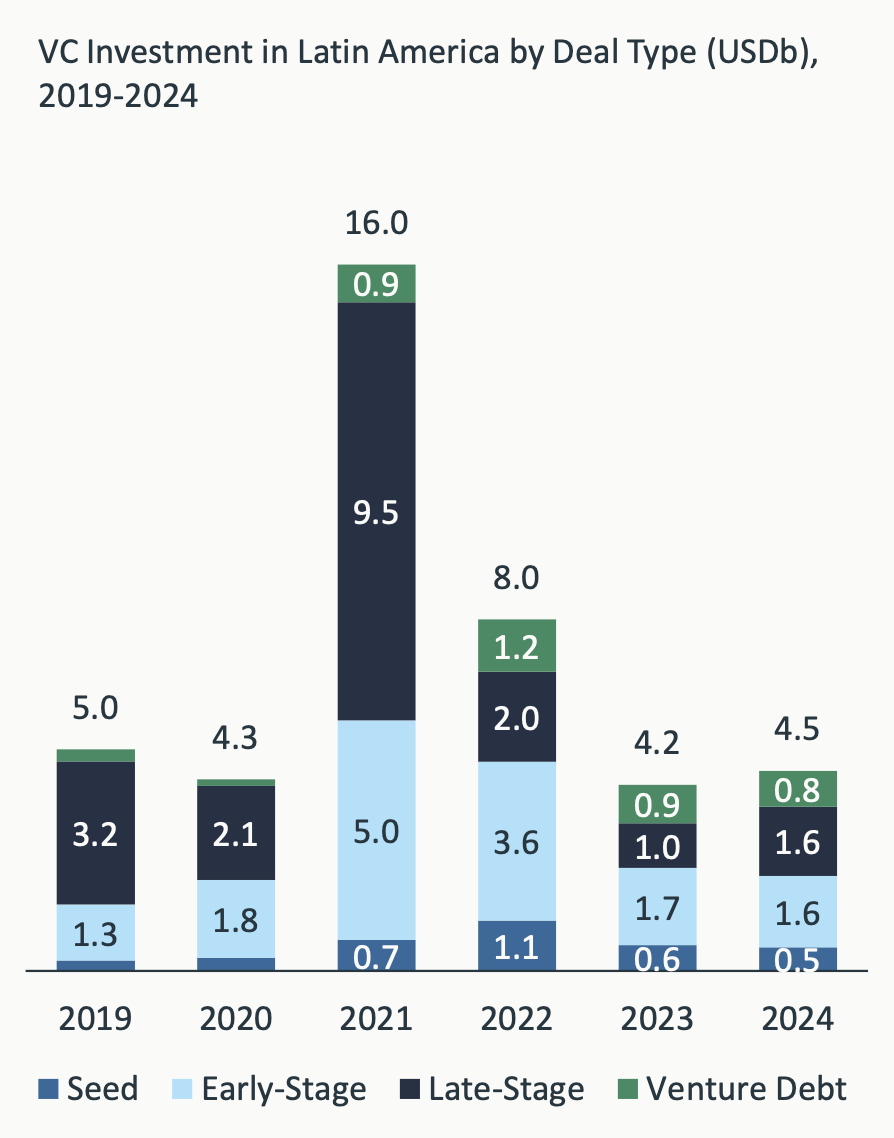

Deal activity remained robust, particularly at the seed and early stages. The total number of deals was significantly higher than in 2019-2020 at similar investment levels, indicating that investors are deploying capital more cautiously and in smaller amounts. While early-stage funding remained a crucial driver, late-stage investment also made a comeback, surging to $1.6 billion—a 55% year-over-year increase—thanks to renewed international investor interest.

Source: LAVCA. Data as of 31 December 2024

Brazil and Mexico Lead the Charge

Brazil and Mexico continued to dominate the region’s venture landscape, capturing 44% and 26% of total venture capital investment, respectively. The data highlights the persistent strength of these two ecosystems, both of which continue to attract a mix of domestic and global capital.

A Shift Towards Profitability and Proven Founders

One of the most notable shifts in the past two years has been the growing emphasis on profitability. Investors are increasingly backing startups with better-perceived risk profiles due to clearer paths to positive cash flow and founder experience, favoring repeat or serial entrepreneurs. These founders accounted for 42% of total capital deployed in 2023 and 2024, compared to just 23% in 2021. This marks a departure from the “growth at all costs” mentality that characterized the boom years.

Sector Trends and Notable Deals

Fintech remains the region’s largest recipient of venture capital dollars, with major late-stage rounds in companies like Ualá ($300M, Argentina), Stori ($212M equity and debt, Mexico), and ADDI ($186M equity and debt, Colombia). The resurgence of venture debt as a complementary financing tool is also worth noting, as companies explore alternative capital structures that are less dilutive for founders and investors.

Source: LAVCA. Data as of 31 December 2024

Cautious Optimism for 2025

While 2024’s stabilization is an encouraging sign, the road ahead is not without risks. Local and regional funds have less dry powder to deploy, given the challenging fundraising environment of the past three years. Additionally, geopolitical uncertainties—particularly policy shifts in the U.S. under Trump’s administration—could impact capital flows into the region in 2025. Potential tariff wars and trade disruptions may introduce volatility, affecting investor sentiment and cross-border transactions.

That said, Latin America’s structural growth story remains intact. The region continues to offer compelling opportunities across fintech, health tech, AI, and climate tech, among others. As global investors recalibrate their emerging market strategies, Latin America’s venture ecosystem appears well-positioned to weather uncertainties with measured optimism as we head into 2025.

good analysis. 2025 could show if we are entering a sustained growth period or not.

LikeLiked by 1 person

Pingback: Aqui estão as maiores startups da América Latina com base na avaliação - TecnoMundo - As Últimas Notícias, Dicas e Reviews de Tecnologia

Pingback: Here are Latin America’s biggest startups based on valuation | TechCrunch

Pingback: How the Post-Pandemic VC Market Is Taking Shape | Latin American VC

Pingback: Evolución del Capital de Riesgo y Ventajas Estratégicas de la Incorporación en EE. UU. – Negocios Globales USA

Pingback: Here are Latin America’s biggest startups based on valuation - America Latina News